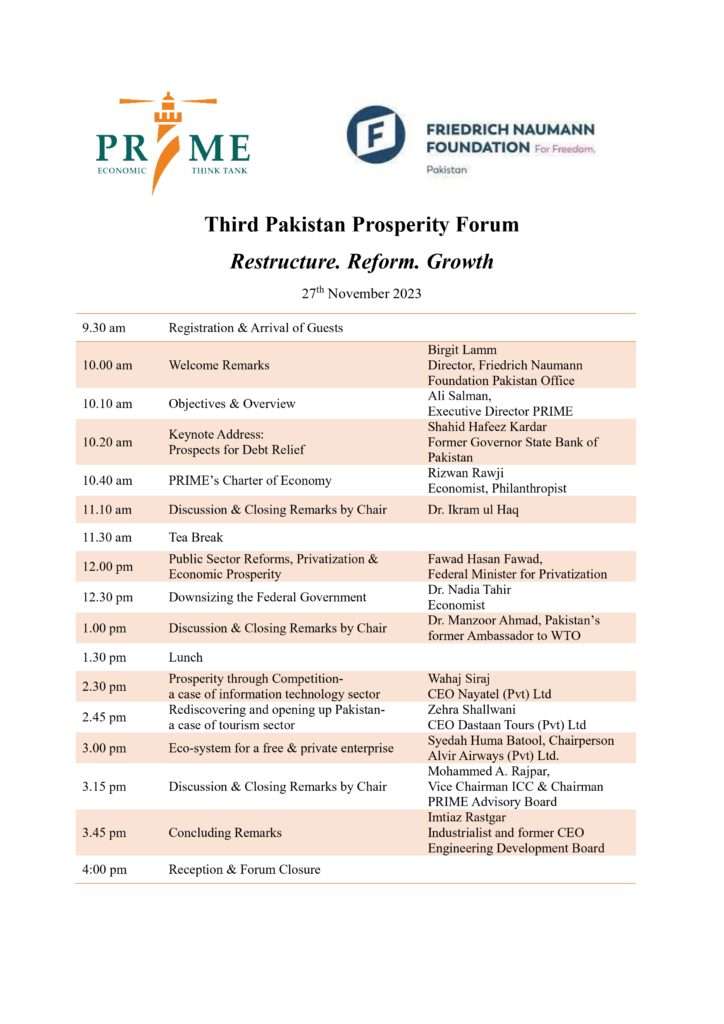

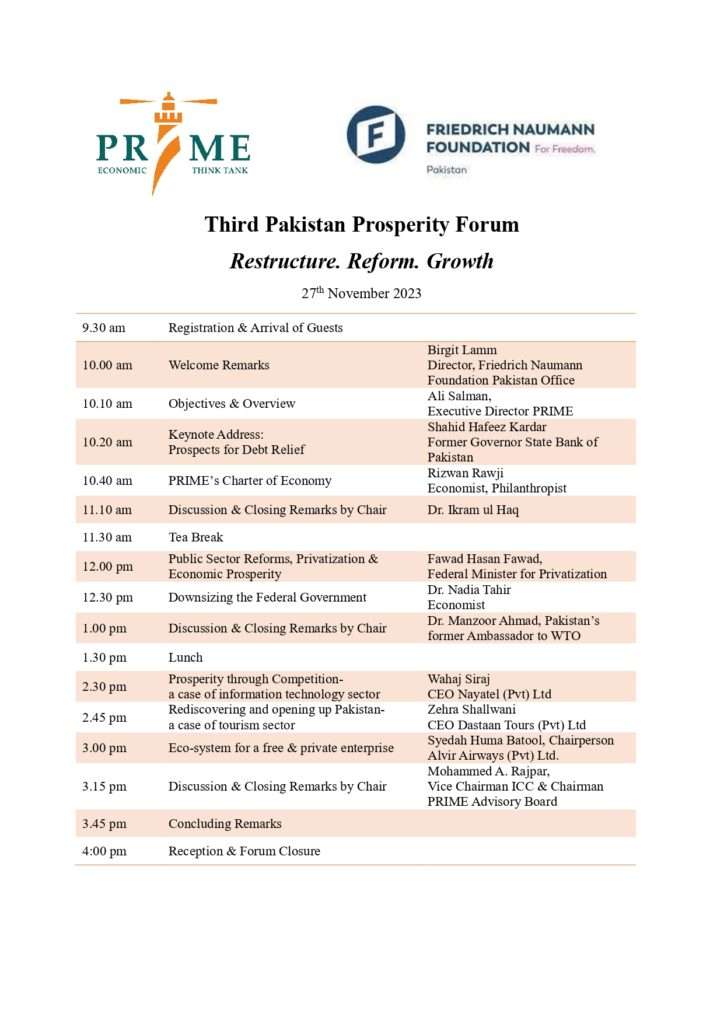

Revamping taxation system and privatizing SOEs are crucial for economic prosperity

![]()

Revamping taxation system and privatizing SOEs are crucial for economic prosperity

The taxation system of Pakistan not only incentivizes people to stay out of the tax system but also contributes to decorporatization, said Mr. Fawad Hasan Fawad – Federal Minister for Privatization, while speaking at the 3rd “Pakistan Prosperity Forum” organized by the Policy Research Institute of Market Economy (PRIME).

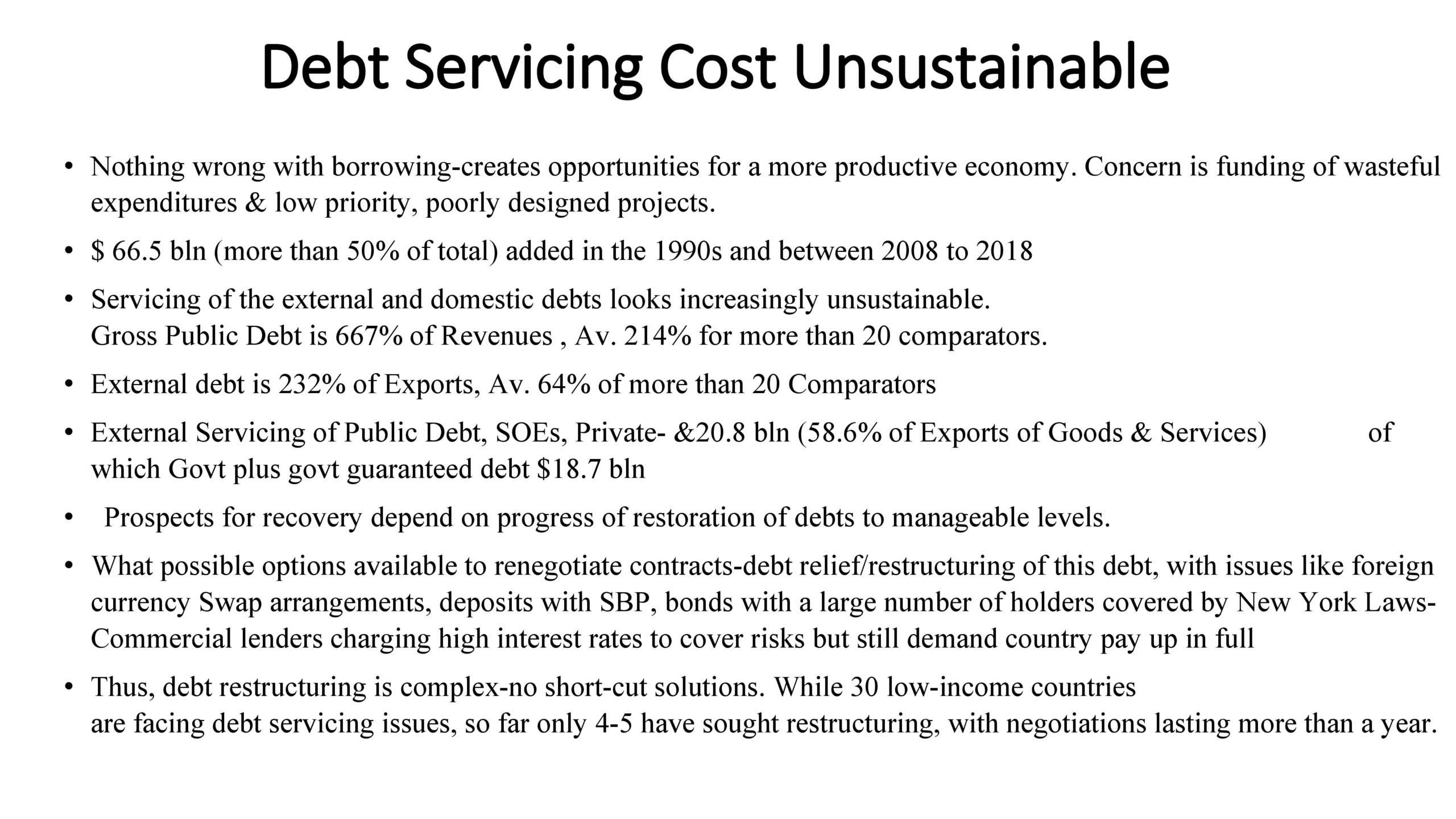

In the keynote address, Mr. Shahid Hafeez Kardar- Former Governor State Bank of Pakistan, highlighted that rationalization of public expenditures is crucial for the sustainability of public finances. Dr. Nadia Tahir stressed upon the importance of fiscal prudence by sharing that fiscal spending has not resulted in economic growth in Pakistan.

The Forum was attended by the representatives of the government, IMF, business community, academia, and media.

Speakers presented the diagnosis of the economic challenges by focusing on the debt crisis caused by unrestrained spending and suggested reforms to build an agenda for sustained economic growth.

Mr. Fawad Hasan Fawad informed the audience that the current state of the public sector is unsustainable and contributes to the deterioration in the business environment in the country. In 3 years from 2018-2021, the government spent Rs. 2.54 trillion in terms of subsidies, grants, and loans to keep commercial SOEs operational. The size of the government has increased by more than three times in the last couple of decades.

Mr. Fawad highlighted the flaws in the country’s taxation system by informing that around 93 percent of the collected tax revenue is either voluntary or withholding; whereas, only 7 percent is actually collected by FBR. Moreover, FBR sends recovery notices to individuals worth billions of rupees while the actual collection is a mere few hundred million. Since 2016, the tax burden on corporate taxpayers has increased by more than 40 percent on average. Such a burden has not only contributed to encouraging people to stay out of the tax system but also decorporatization.

The public sector reforms should include bureaucratic reforms and taxation system reforms. These two areas are crucial for improving performance of the state. He stressed that the reform should not increase in the size of the federal and provincial governments, and the power of state functionaries. The reforms also need to focus on building the capacity of the state to regulate markets from where the government exists and the private sector takes over.

Mr. Shahid Hafeez Kardar highlighted that the wasteful expenditures on low-priority, and poorly designed projects have made the debt unsustainable. While addressing the Forum, Mr. Kardar said that borrowing is not harmful if utilized in productive activities and generating assets. He informed that Pakistan’s Gross Public Debt is 667 percent of revenues, and external debt is 232 percent of exports.

The overhaul of the economy requires rationalization of government expenditures, moving towards a contributory pension system, reducing the footprint of the government in the economy, rationalizing tariff structure by phasing out protection of industries and revamping the taxation system by reducing the rates and number of taxes.

Mr. Rizwan Rawji – Businessmen, presented the Charter of Economy prepared by PRIME and highlighted that political stability and strong political will hold critical importance in promoting economic prosperity. The economic woes such as the balance of payment crisis, unsustainable debt, and inflation are only due to misaligned fiscal policies of the governments. Currently, out of 5 million tax filers, less than 3 million pay tax, and a significant portion of sales tax is collected from a mere 400 entities. Mr. Rawji suggested that reforms envisaged in the Charter of Economy are based on the pillars of economic prosperity, which are: low and broad-based tax rates, spending restraints, low footprint of the government in the economy, privatization of loss-making SOEs, tariff rationalization, and sound money.

Mr. Ali Salman – Executive Director PRIME, remarked that the size of the government and its presence in the economy need to be reduced to improve fiscal sustainability and create an enabling business environment in the country.

The speakers had a consensus that reforms should start from the restructuring and resizing of the government to reduce its presence in the economy. The reforms should be complemented by restricting the public spending and focusing on revamping the taxation system by reducing the number and rates of taxes to broaden the tax base.

For inquiries, please contact farhan@primeinstitute.org or call +92 (51) 8 31 43 38

Without structural reforms, SIFC will not succeed

![]()

Without structural reforms, SIFC will not succeed

The mandate of Special Investment Facilitation Council (SIFC) neither include institutional reforms nor simplification of procedures despite the acknowledgement that complexity of business regulations and bureaucratic hurdles are the reasons behind dismal state of economy.

Reforms should start from the government departments to create ease for the Pakistani entrepreneurs and improve provision of public services instead of creating new councils and adding more complexities. Creation of a parallel body to expedite the decision making process and requisite approvals may not be a sustainable solution until the concerned government departments are reformed.

PRIME has published its quarterly assessment report, PRIME Plus October 2023, which analyzes the efficacy of the Special Investment Facilitation Council (SIFC), the macroeconomic performance of the country in Q1- FY2024, and potential challenges.

The report scrutinizes the establishment of SIFC which the government has proclaimed as its “Plan B” to overcome the recurring balance of payment (BoP) crises by attracting foreign investment in the country. SIFC has identified projects in 4 sectors: Agriculture, Mining and Minerals, I.T., and Energy. The establishment of SIFC under the umbrella of the BOI with separate management and objectives highlights the acknowledgment of the failure of BOI by the government and the need to have an alternative body.

The report “Prime Plus” concludes that the efficacy of SIFC as a “Plan B” needs to be evaluated meticulously. The inefficiency of BOI has failed to prompt the government towards carrying out institutional and regulatory reforms that have been responsible for the reluctance of foreign investors. The establishment of SIFC indicates that the government has neglected to address the bureaucratic hurdles and associated inefficiencies.

The report highlights that the policy environment of the country is unconducive for business growth. The

frequent changes and the repetition of ineffective policies have weakened the interest

of foreign investors.

The local business community is excluded from the decision-making process and no effort has been made to mobilize domestic resources. The structure and objectives of SIFC are unclear. Moreover, higher involvement of the military in decision-making and implementation will not be help to restore investment climate, which require deregulation and tax reforms.

The country’s economic performance has remained unsatisfactory while external financial obligations continue to mount. Against the target of 3.2 percent GDP set by the government, international financial institutions have downgraded their forecasts to around 2 percent. On the external front, the financial obligations in FY 2024 are around $28 billion. On the domestic front, the government faces a significant financial burden as 79 percent of the expected FBR revenues will be spent on debt servicing while leaving little space to carry out other expenditures.

Inflation continues to remain a challenge and people have experienced an exponential fall in their purchasing power. The CPI inflation stood at 31.4 percent in September 2023 while average CPI inflation in Q1 FY 2024 cloaked at 29 percent. The government’s decision to pass on the cost of utilities to the consumers without addressing policy and institutional inefficiencies may prove to be futile and keep inflation unanchored.

The political environment in the country remains uncertain as the schedule of elections is still not announced by the Election Commission and rumors about delays continue to prevail. Political stability is likely to improve when elections are announced. The crackdown started by the government against deviants in the currency and gold markets to curtail smuggling will not bear fruit unless policy uncertainties are addressed.

For inquiries, please contact farhan@primeinstitute.org or call 0331-5226825

Tax Payers Alliance Pakistan (TPAP) submits Proposals to Task Force on Tax & FBR Reforms

Tax Payers Alliance Pakistan (TPAP) submits Proposals to Task Force on Tax and

FBR Reforms

TPAP| October 24, 2023

Federal Board of Revenue (FBR) constituted a Task Force on Tax & FBR Reforms vide notification dated 27th September, 2023. The purpose of this Task Force is to suggest measures regarding the improvement of FBR efficiency. As per TORs of the Task Force, it will review FBR & tax collection data, performance indicators, and access to data. It will also address tax evasion, smuggling, and corruption, propose structural reforms for the tax administration, and suggest technology-based measures to enhance tax collection. It will analyze tax policy, examine tax expenditures, and recommend the use of information technology for better compliance and transparency. The Task Force will submit a comprehensive report to the Government, outlining revenue and policy reform measures, including potential changes in tax administration and laws.

Tax Payers Alliance Pakistan (TPAP) – an initiative of economic think tank PRIME, in order to discuss and deliberate on related issues called a meeting of its members on 6th October 2023, who participated actively to share their ideas to be presented to the Task Force. On the basis of said meeting, TPAP

finalized proposals and submitted to the Task Force on 19th October, 2023. Proposals submitted by TPAP aim at reforming the taxation system in Pakistan to promote simplicity, transparency, and compliance; to eliminate taxes that are unjustified, discriminatory and have become redundant; and to create a fairer and more efficient tax system in Pakistan that can provide sustainable funding for public expenditures.

TPAP, the brainchild of PRIME, developed these proposals in consultation with its members, comprising of tax experts, development consultants, researchers, scholars, people from business community and salaried individuals from across Pakistan. The meeting was led by Mr. Ali Salman, Executive Director PRIME, Mr. Anas Farhan, Convener TPAP Secretariat Islamabad and Mr. Usman Azmat, Convener TPAP Lahore Chapter.

[pdf-embedder url=”https://primeinstitute.org/wp-content/uploads/2023/10/TPAP-proposals-submitted-to-Task-Force-on-Tax-FBR-Reforms.pdf” title=”TPAP proposals submitted to Task Force on Tax & FBR Reforms”]

Incredible things happen when taxpayers come together and raise their voice to bring betterment in the taxation system.

Click below to get the full meeting rundown.

- « Previous Page

- 1

- …

- 4

- 5

- 6

- 7

- 8

- …

- 30

- Next Page »